Ceramic Wall Tiles Market Growth & Trends

The global ceramic wall tiles market size is expected to reach USD 240.9 billion by 2030, registering a CAGR of 7.8% from 2023 to 2030, according to a new report by Grand View Research, Inc. Ceramic wall tiles are gaining high demand from residential and commercial applications to replace traditional wall covering materials including paint and wallpapers. Easy accessibility, superior dirt & heat resistance, and affordable pricing of these products are likely to drive the market.

Ceramic wall tiles are finding increasing adoption in newer residential application settings, such as living rooms, lobby, and bedrooms, on account of their low cost, low maintenance, and high durability. Rising demand for ceramic wall tiles as a cost-effective alternative to conventional stone materials, such as granite and marble, is likely to propel their demand in commercial constructions including corporate offices, hotel lobbies, and museums.

Ceramic tiles are considered to be eco-friendly as they are completely manufactured using natural materials, such as clay and sand, along with other recycled materials. Moreover, these wall tiles also help in reducing energy utilization in modern constructions on account of their insulating properties. Growing demand for environmentally sustainable building materials is expected to generate a progressive demand for the product.

Consumers are experimenting with design, colors, and patterns to ensure a unique look of building structures. As a result, manufacturers are compelled to adopt advanced printing and production technologies to develop modern designs and textures. Product variation, tile quality, and unique designs coupled with established distribution networks are expected to be the key factors favoring growth of the major market players.

Request a free sample copy or view report summary:

Ceramic Wall Tiles Market Report

Ceramic Wall Tiles Market Report Highlights

- The healthcare application segment is expected to expand at a CAGR of 7.6% over the projected period, in terms of revenue.

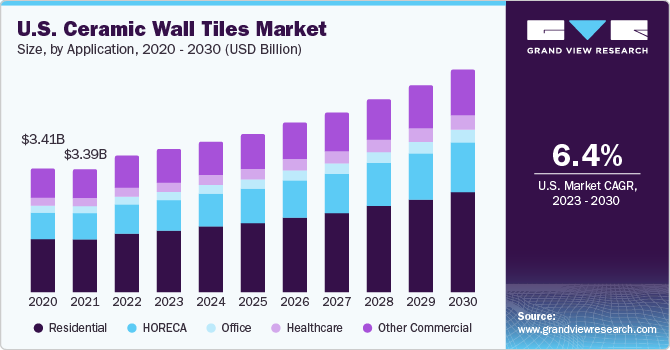

- The residential segment accounted for the largest revenue share of 44.0% in 2022 in the ceramic wall tiles market and is expected to expand at the fastest CAGR of 8.4% during the forecast period.

- The rapid growth of the tourism industry in the Asia Pacific region has resulted in the strong expansion of the HORECA segment, owing to healthy growth of tourism industry in the UAE, Saudi Arabia, and Egypt

- The market players are likely to target the developing markets such as India, China, and Southeast Asian countries to tap the robust market opportunities resulting from the rapid growth of construction sector.

Key Ceramic Wall Tiles Company Insights

The market is characterized by the presence of both small-scale and large-scale players, resulting in an intense level of competition. China, India, Spain, Italy, and Brazil have emerged as global manufacturing hubs for ceramic tiles. On the other hand, developed countries, such as the U.S., the U.K., and Germany, are largely dependent on imports to address product demand.

Market players are undertaking several innovative initiatives and awareness campaigns to educate consumers regarding the advantages of ceramic wall tiles over traditional materials such as paints and wallpapers. For instance, the Tile Council of North America coordinated the Why Tile campaign launched in April 2017, with the primary aim of educating consumers about the benefits and positive aspects of ceramic tiles.

Industry players are developing lightweight products in large sizes and with smaller thickness. They are also investing in training programs for contractors for installing extra-large tiles. Furthermore, market players showcase their product portfolios through various exhibitions, such as Coverings, Cersaie, and CeramBath, to increase product adoption in end-use applications.

Key Ceramic Wall Tiles Companies:

- Porcelanosa Grupo A.I.E.

- Panariagroup Industrie Ceramiche S.p.A.

- Mohawk Industries, Inc.

- Kajaria Ceramics Limited

- China Ceramics Co., Ltd.