The global immunohistochemistry market size is estimated to reach a value of USD 3.1 billion by 2025, according to a new report by Grand View Research, Inc. It is anticipated to witness a revenue-based CAGR of 8.8% over the forecast period. High prevalence of cancer and increasing healthcare expenses driven by expanding aging population base are recognized as the most influential factors driving the market.

Cancer has high morbidity and mortality risk. Diagnosis of this disease majorly depends on the stage of the disease at admission. This has led to high demand of immunohistochemistry (IHC) products. IHC staining process is performed on cancer tissues to reveal the presence of HER2 receptors and/or hormone receptors on their surface. This information plays a vital role in planning cancer treatment. This factor is anticipated to drive demand in near future. In addition, rising popularity of targeted immunotherapy and biologic therapy for anticancer drug development and increasing Food and Drug Administration (FDA) approvals are expected to boost market growth in near future.

Significant rise in healthcare spending and shift in focus on value-based healthcare solutions can further impel growth of the immunohistochemistry market over the forecast period. According to the Centers of Medicare & Medicaid Services (CMS) projections, the National Health Expenditure is anticipated to rise at an average of 5.5% every year from 2017 to 2026. It is expected to reach around USD 5.7 trillion by 2026. Hospitals and care facilities are adopting a more specific and targeted therapy for better outcomes and to establish a move value-based healthcare delivery.

“Read Report Summary, Toc, Market Segmentation, Research Methodology, Request a Free Sample“ Click the link below:

Further key findings from the study suggest:

- Antibody segment accounted for the largest market share due to rising regulatory approvals for therapeutic antibody products

- North America registered the highest CAGR in 2017 owing to well-established healthcare infrastructure and favorable reimbursements

- APAC is expected to witness the fastest CAGR owing to increasing healthcare expenses and aging population

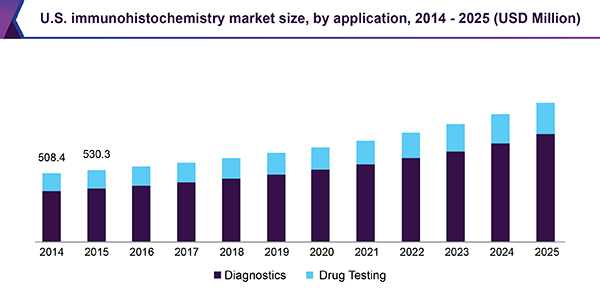

- Diagnostics segment dominated the immunohistochemistry market in 2017 owing to high prevalence of cancer and other such chronic diseases

- Hospitals and diagnostic laboratories is anticipated to exhibit significant CAGR over the forecast period due to increasing disease prevalence and high number of these facilities with advanced infrastructure

- Some of the key market players are Abcam plc; Agilent Technologies; Bio-Rad Laboratories, Inc.; Cell Signaling Technology, Inc.; Danaher Corporation; Merck KGaA; PerkinElmer, Inc.; and Thermo Fisher Scientific, Inc.

“Would you like/try a Free Sample Report” Click the link below:

Grand View Research has segmented the global immunohistochemistry market on the basis of product, application, end use, and region:

Immunohistochemistry Product Outlook (Revenue, USD Million, 2014–2025)

- Antibodies

- Primary Antibodies

- Secondary Antibodies

- Equipment

- Slide Staining Systems

- Tissue Microarrays

- Tissue Processing Systems

- Slide Scanners

- Others

- Reagents

- Histological Stains

- Blocking Sera and Reagents

- Chromogenic Substrates

- Fixation Reagents

- Stabilizers

- Organic Solvents

- Proteolytic Enzymes

- Diluents

- Kits

Immunohistochemistry Application Outlook (Revenue, USD Million, 2014–2025)

- Diagnostics

- Cancer

- Infectious Diseases

- Cardiovascular Diseases

- Autoimmune Diseases

- Diabetes Mellitus

- Nephrological Diseases

- Drug Testing

Immunohistochemistry End Use Outlook (Revenue, USD Million, 2014–2025)

- Hospitals and Diagnostic Laboratories

- Research Institutes

- Others