2D Barcode Reader Market Revenue Reach $8.6 Billion | Global Industry Report Forecast 2025 | Market Research Report

The global 2D barcode reader market size is expected to reach USD 8.60 billion by 2025, registering a CAGR of 4.7% over the forecast period, according to a new report by Grand View Research, Inc. The market is expected to grow as incumbents of industries, such as retail, transportation & logistics, warehousing, and e-commerce, continue to adopt various tools to increase the operational efficiency of their business operations. Initiatives being undertaken by businesses to develop innovative strategies and adopt strategic methods and tools to gain a competitive edge in the marketplace also bode well for the growth of the market.

A barcode reader is emerging as one of the solutions that can potentially help businesses in ensuring lean operations and improving productivity. As a result, manufacturers operating in the market are responding to the situation by focusing on the development of innovative technologies for enhancing the barcode reading capabilities and offering numerous benefits to several end-use industries. The development of 2-Dimensional (2D) barcode scanners has particularly helped in solving several problems and challenges, such as having the capability to scan 2D barcodes while also ensuring the backward compatibility to scan 1-Dimensional (1D) barcodes.

A 2D barcode reader has assumed a pivotal role in increasing the operational efficiency of businesses. Owing to advantages such as higher accuracy, higher scanning speed, reduction in clerical cost, and improvement in customer service, the 2D barcode reader has cemented its position as a prominent tool for streamlining internal and external operations. Apart from being compact and flexible, the reader can also turn out to be an economical solution with a payback period of just 3–6 months. It is particularly getting vital for the industrial sector as a result.

The adoption of barcode technology as an automatic identification/scanning system has helped significantly in reducing human errors. A typical error rate for human data entry is estimated at around 1 error per 300 characters typed. However, the error rate of a barcode reader is estimated at 1 error per 35 trillion characters. Thus, from accelerating the checkout process in the retail industry to tracking inventories in warehouses, barcode scanners have eventually proliferated into a myriad of business operations. These scanners can not only help businesses in conserving their resources but in optimizing the data entry process, improving real-time visibility of the products, and enhancing the productivity of employees.

However, the proliferation of mobile barcode Software Development Kits (SDKs) is anticipated to hinder the growth of the market. Organizations with low-volume operations are particularly preferring smartphones over scanners for barcodes to reduce their operational costs. The adoption of Bring Your Own Device (BYOD) policies is also anticipated to encourage the adoption of barcode scanning apps over readers. In other words, any growth in the usage of smartphones for scanning barcodes can potentially take a toll on the demand for dedicated 2D barcode readers.

“Read Report Summary, Toc, Market Segmentation, Research Methodology, Request a Free Sample“ Click the link below:

Further key findings from the report suggest:

- The global market for 2D barcode reader was valued at USD 6.39 billion in 2018 and is expected to exhibit a CAGR of 4.7% from 2019 to 2025

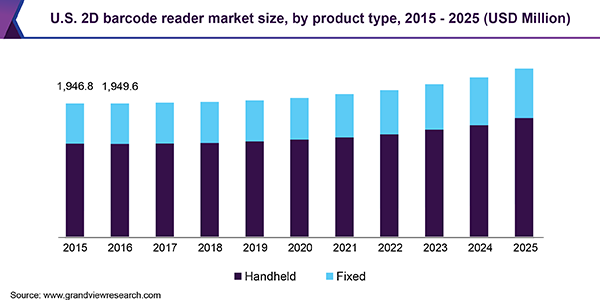

- The handheld segment accounted for the largest revenue share of over 65% in 2018 and is anticipated to register a CAGR of 5.2% over the forecast period

- The logistics segment is anticipated to exhibit the highest CAGR of 6.1% over the forecast period as transporters continue to deploy barcode readers at their logistics facilities

- The warehousing segment dominated the market in 2018 and was valued at USD 2.60 billion as warehousing companies aggressively adopted 2D barcode readers to track inventories

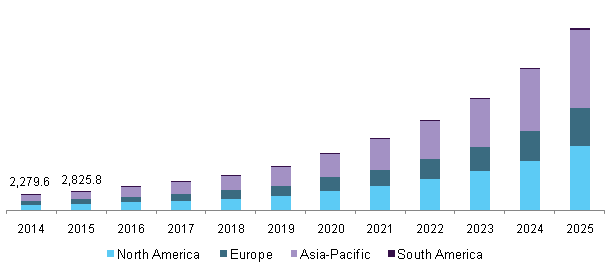

- The Asia Pacific regional market was valued at USD 2.66 billion in 2018 and is expected to register a significant growth rate owing to the booming e-commerce industry and the continued rollout of warehousing network, particularly in developing countries, such as India and China

- The key players dominating the 2D barcode reader market include Zebra Technologies Corporation, Datalogic S.p.A., Cognex Corporation, Honeywell International Inc., and Keyence Corporation, among others

Grand View Research has segmented the global 2D barcode reader market on the basis of product type, application, and region:

2D Barcode Reader Product Type Outlook (Revenue, USD Million, 2015–2025)

- Handheld

- Fixed

2D Barcode Reader Application Outlook (Revenue, USD Million, 2015–2025)

- Warehousing

- Logistics

- E-commerce & Retail