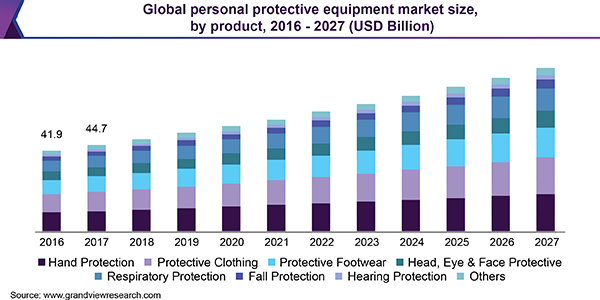

The global industrial protective clothing market size is expected to reach USD 22.57 billion by 2025, according to a new report by Grand View Research, Inc. It is anticipated to expand at a CAGR of 13.7% during the forecast period. Increasing awareness pertaining to health and safety of workers across various industries, including chemical, construction, and manufacturing is likely to drive the growth.

Favorable regulatory scenario to minimize occupational hazards at the workplace is expected to be the key factor positively influencing the market growth. Furthermore, rapid industrialization and urbanization in developing economies, which demands higher workforce, is expected to fuel the demand for industrial protective clothing over the projected period.

Rising health concerns owing to exposure to harmful emissions and smoke coupled with increasing mishaps, particularly in oil and gas and mining industry are likely to support the product demand. Increasing number blue-collar workforce in construction and manufacturing industries is further projected to propel the demand for protective clothes over the forecast period.

The market players engage in continuous R&D to produce multi-functional protective clothing, with high durability to cater to the growing demand. Furthermore, the companies emphasize on manufacturing clothing which can comply with the guidelines given by the Occupational Safety and Health Administration (OSHA), in order to sustain in the market.

To request a sample copy or view summary of this report, click the link below:

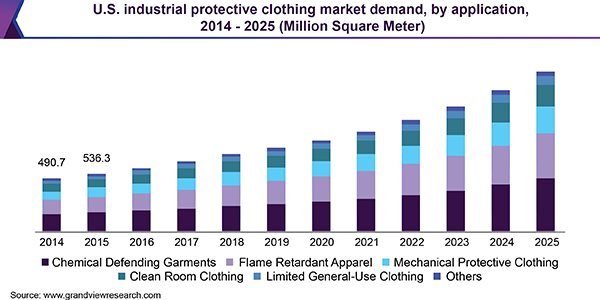

Further key findings from the report suggest:

- Demand for durable protective clothing is expected to reach USD 11.50 billion by 2025, on account of the re-usability and superior heat and chemical resistance properties of the product

- Chemical defending garments is expected to expand at a CAGR of 13.9% over the forecast period owing to rising concerns regarding workforce health safety against harmful and hazardous substances and radiations in chemical and nuclear industries

- Demand for disposable chemical defending garments is expected to witness significant growth on account of their rising demand in chemical laboratories and R&D centers

- North America accounted for 41.4% of the global market share in 2018, as the industries in the region need to comply with the stringent regulations and guidelines given by the authorities such as OSHA, NFPA, and ASTM

- Growing application industries such as construction, mining, chemical, and food in Asia Pacific is expected to drive the industrial protective clothing market over the forecast period

- In 2018, Germany accounted for the highest market share in Europe, on account of well-established manufacturing facilities for automotive, chemical, and power generation sector

- Technological advancements to introduce multilayers and coatings with attractive designs is likely to be the key factor defining success for the market players

Grand View Research has segmented the global industrial protective clothing market on the basis of product, application, and region:

Industrial Protective Clothing Product Outlook (Volume, Million Square Meters; Revenue, USD Million, 2014–2025)

- Durable

- Disposable

Industrial Protective Clothing Application Outlook (Volume, Million Square Meters; Revenue, USD Million, 2014–2025)

- Flame Retardant Apparel

- Chemical Defending Garments

- Radiation Protection

- Particulate Matter

- Clean Room Clothing

- Mechanical Protective Clothing

- Limited General-Use Clothing

- Others