Brushless DC Motor Market Growth & Trends

The global brushless DC motor market is expected to reach USD 30,862.4 million by 2030, registering a compounded annual growth rate (CAGR) of 6.5% from 2024 to 2030, according to a study conducted by Grand View Research, Inc. These motors are thermally resistant, require low maintenance, and operate at low temperatures, eliminating any threat of sparks. Low-cost maintenance, high efficiency at lower costs, and the rising adoption of Electric Vehicles (EVs) are some of the key factors driving the product demand over the forecast period.

The emergence of sensor-less controls for brushless DC (BLDC) type is likely to boost the durability and reliability of the product, thereby reducing the number of mechanical misalignments, electrical connections, as well as the weight and size of the end product. These factors are further estimated to drive market growth over the forecast period. Furthermore, the growing production of vehicles, globally, to cope up with the rising demand is anticipated to have a positive impact on the market growth.

The product is extensively used in motorized vehicle applications, such as in sunroof systems, motorized seats, and adjustable mirrors. In addition, these powertrains are extensively being preferred for performance applications in vehicles, such as chassis fittings, power-train systems, and safety fittings, owing to simple structure, fewer maintenance requirements, and extended operational life. Thus, increasing product adoption by the automobile industry for multiple applications is anticipated to drive the market over the forecast period.

Rising product usage in EVs in mechatronic systems, primarily in batteries for accumulators and power electronic converters, owing to advantages, such as high operating speed, compact size, and quick response time, will also augment the market growth. The production of EVs is on the rise, globally, supported by government initiatives to encourage the usage of non-conventional fuels and effectively reduce the adverse impacts of carbon emissions. Thus, the increasing EV production is anticipated to directly influence the product demand over the forecast period.

Request a free sample copy or view report summary:

Brushless DC Motor Market Report

Brushless DC Motor Market Report Highlights

- The brushless DC motor is expected to grow significantly on account of the benefits of these motors such as durability, low power consumptions, and less maintenance.

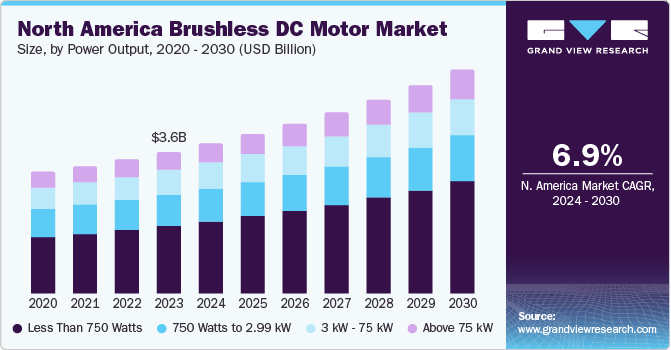

- Less than 750 watt brushless DC motor segment is expected to witness rapid growth from 2024 to 2030, which can be primarily ascribed to their extensive applications in numerous motor vehicles and household devices applications.

- Motor vehicles extensively use these for variety of applications. Increased production of automobiles and e-vehicles across the globe is anticipated to positively impact the growth of motor vehicle segment over the forecast period.

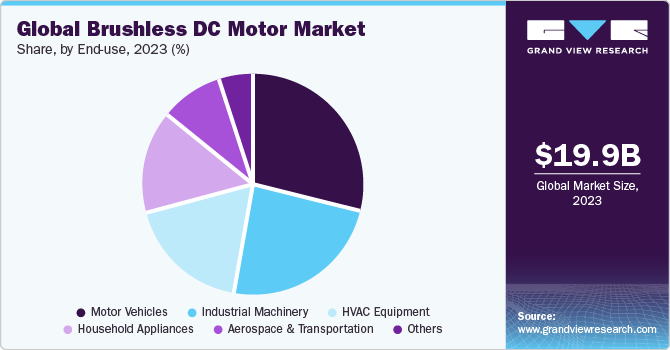

- The industrial machinery segment held 24% of the global market in 2023. Numerous industrial machines deploy brushless DC motors owing to advantages offered such as high efficiency, low power consumption and low maintenance costs among others.

- Asia Pacific is expected to emerge as the fastest-growing regional market, whilst registering a CAGR exceeding 7.8% from 2024 to 2030. Increasing industrialization in developing nations such as China, India and South Korea has fueled the adoption of brushless DC motor in the region.

- The key players capturing major market share include ABB Ltd, Ametek Inc., Johnson Electric and Nidec Motor Corporation, among others. Numerous companies are focusing on developing low-maintenance and eco-friendly products in order to gain a competitive edge.

Brushless DC Motor Market Segmentation

Grand View Research has segmented the global Brushless DC Motor Market report based on rotor type, power, speed, end-use, and region

Brushless DC Motor Rotor Type Outlook (Revenue, USD Million, 2017–2030)

- Inner Rotor

- Outer Rotor

Brushless DC Motor Power Output Outlook (Revenue, USD Million, 2017–2030)

- Less than 750 Watts

- 750 Watts to 2.99 kW

- 3 kW — 75 kW

- Above 75 kW

Brushless DC Motor Speed Outlook (Revenue, USD Million, 2017–2030)

- Less than 500 RPM

- 501–2,000 RPM

- 2,001–10,000 RPM

- More than 10,000 RPM

Brushless DC Motor End-use Outlook (Revenue, USD Million, 2017–2030)

- Industrial Machinery

- Motor Vehicles

- Safety

- Comfort

- Performance

- HVAC Equipment

- Aerospace & Transportation

- Household Appliances

- Others

Brushless DC Motor Regional Outlook (Revenue, USD Million, 2017–2030)

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Latin America

- Brazil

- Mexico

- Middle East and Africa (MEA)

- Kingdom of Saudi Arabia (KSA)

- UAE

- South Africa

List of Key Players of Brushless DC Motor Market

- ABB

- Ametek Inc.

- Johnson Electric Holdings Limited.

- NIDEC CORPORATION

- Allied Motion Technologies, Inc.

- WorldWide Electric

- Schneider Electric

- Regal Rexnord Corporation

- Siemens

- TECO Corporation

- MinebeaMitsumi Inc.

- ORIENTAL MOTOR USA CORP