The global wireless health market size is expected to reach USD 315.4 billion by 2025, according to a new report by Grand View Research, Inc., exhibiting a 23.5% CAGR during the forecast period. An increase in the number of eHealth initiatives worldwide, an increase in the penetration of smartphones and Internet connectivity, and growth in the trend of self-disease management are some of the factors boosting the market growth. A growing trend toward the use of wearable devices for monitoring physical parameters, such as sleep, blood pressure, heart rate, and physical activity, is also driving the wireless health market.

The growing geriatric population and subsequent rise in chronic disease burden is also driving the market. According to The Wall Street Journal, there has been an increase in the usage of digital medicine, which enables the management of chronic conditions such as diabetes, heart diseases, and respiratory diseases. Moreover, these digital medicines are cost-effective alternatives to traditional disease management.

Shifting trend toward value-based care is another factor contributing to the growth of the wireless health market. At present, some of the telehealth services, such as consulting a doctor via video connection, are reimbursed by CMS. The use of digital services such as various platforms for health management has promoted the development of various applications for managing diabetes, heart diseases, and asthma. The use of applications for chronic disease management, fitness tracking, supporting medication adherence, preventing hospital readmissions, symptom tracking, and managing mental and behavioral health are on the rise.

Further key findings from the report suggest:

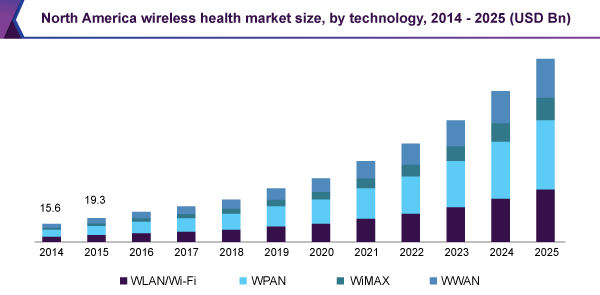

- Wireless Personal Area Network (WPAN) emerged as the largest technology segment and Wireless Wide Area Network (WWAN) is anticipated to witness the fastest growth over the coming years

- Software emerged as the largest component segment owing to the rise in the number of research initiatives. The services segment, on the other hand, is anticipated to expand at the fastest CAGR of 24.7%

- Patient-specific applications emerged as the largest segment owing to increase in adoption and rise in research initiatives for developing them to manage individual health

- The patient segment accounted for the largest revenue share in terms of end use owing to the increase in the use of health and fitness applications by people around the world

- The market is highly fragmented with participants such as IBM; Allscripts; Cerner Corporation; Omron Corporation; Koninklijke Philips N.V.; Epic Systems Corporation; and Evolent Health, Inc.