May 2020 | Report Format: Electronic (PDF)

The global molecular diagnostics market size is expected to reach USD 18.2 billion by 2027, according to a new report by Grand View Research, Inc., registering a CAGR of 9.0% over the forecast period. Increasing prevalence of infectious diseases such as influenza and human papillomavirus is projected to be the key factor the growth of the market.

In the underdeveloped regions of Africa, increasing instances of infections such as tuberculosis and HIV have been witnessed in the last few years. This is projected to drive the demand for accurate and early diagnostic techniques to curb the spread of these infections.

Rapid technological advancements-leading to accurate results, portability, and cost-effectiveness-are expected to be a high impact rendering driver for this market. Companies are upgrading their products by implementing new techniques to gain specific and accurate results. Companies such as Sigma Aldrich Corporation and Qiagen are developing a new range of molecular diagnostic techniques, such as Transcription-Mediated Amplification (TMA) and Loop-Mediated Isothermal Amplification (LAMP), for the diagnosis of tumors.

Key players in the market are adopting various marketing strategies such as collaborations with technologically advanced companies and diagnostic centers. Furthermore, players are focusing on expanding their geographic presence in order to increase their market share.

To request a sample copy or view summary of this report, click the link below:

www.grandviewresearch.com/industry-analysis/molecular-diagnostics-market

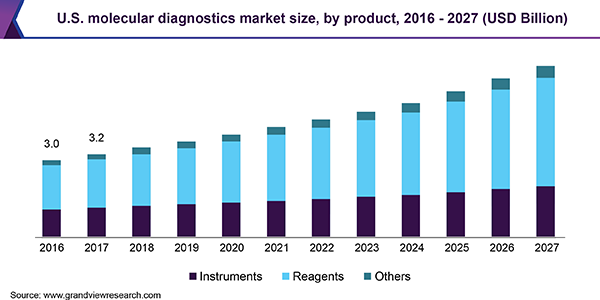

Further key findings from the report suggest:

- Reagents dominated the market in 2019 and is also projected to be the fastest-growing product segment owing to its high adoption in research and clinical settings. Standard reagents also provide efficient and accurate results

- Instruments such as next generation sequencing platforms and PCR are increasingly preferred by diagnostic institutes and central laboratories as these tests deliver reliable and quick results and are suitable for a number of diagnostic procedures

- Central laboratories emerged as the leading test location for molecular diagnostics in 2019. This is attributed to the availability of skilled labor and well-established infrastructure

- Point-of-care is expected to be the fastest-growing segment over the forecast period owing to increase in demand for bedside testing, accuracy of results, and rise in healthcare awareness

- Infectious diseases were the largest revenue generating segment in 2019 as molecular diagnostics offer clinicians with better substitutes to diagnose numerous infectious pathogens, bacteria, and virus in a short time while producing extremely accurate results

- The oncology segment is projected to exhibit a CAGR of around 11.3% over the forecast period owing to increasing awareness amongst patients and healthcare professionals regarding available technologies such as molecular testing for cancer diagnosis

- On the basis of technology, PCR was the largest revenue generating segment in 2019 owing to factors such as growing applications of multiplex PCR and commercialization of easy-to-use PCR-based molecular diagnostic kits

- North America was the largest revenue generating region in 2019, followed by Europe. Key factors attributing to their dominance are high patient awareness levels, sophisticated healthcare infrastructure, growing healthcare expenditure, and high R&D pertaining to drug discovery and development

- Some of the major players operating in molecular diagnostics market are F. Hoffmann-La Roche Ltd; Siemens Healthcare GmbH; Bio-Rad Laboratories, Inc.; Novartis AG (Grifols); Danaher Corporation; Alere, Inc.; Sysmex Corporation; bioMérieux SA; Becton, Dickinson and Company; Hologic, Inc. (Gen Probe); Johnson & Johnson Services, Inc.; Bayer AG; Cepheid; Dako; and Qiagen.